Contact Us

Write to us to start cooperation or ask the

questions. We respond within 1 hour

Dear colleagues

I am in the consulting business all my career. From technical consulting (civil engineering) to digital (software development & testing) to process re-engineering (as we use to call Lean Engineering in the eighties) to Management Consulting, to technology/software based Business Transformation and finally FINTECH Consulting. I accumulated over the years most of the degrees one can have in our field from Project Management to Lean Engineering to Behavioural Analysis to Organisation Studies.

But despite the decades of experience and studies every new breakthrough in our field keeps exciting me. There have been plenty recently. It is a new brave word out there now. Established practices are shaken up and new services come into existence daily. Services that open new possibilities, create new paradigms and affect the way we thought business practices. It all started in the B2C and P2P FINTECH space and fairly recently in the B2B and B2B2B....G2C or B2B2B...2B2C, where G stands for a Government or Public Organisation, B for Business and C for Consumer.

This was not an accident. Innovators choose these fields because, as it is well documented, 9 out of 10 business problems that affect the bottom line derive from the way companies transact, from deficiencies within their business transaction practices.

By default all business functions involve transactions, from their strategy, to internal processes, to their operations. (I mean a transaction as an agreement, communication or movement or all three at the same time, between a “buyer” and a “seller” to exchange an asset for a reward.)

How much one will sell a product or service, to whom, how, in which currency and with what terms, how much he will buy, from whom, how, in which currency and with what terms everything he needs to produce his product or deliver his services, how one will remunerate his personnel in which currency and in which terms and so forth, everything is a transaction and is crucial.

As businesses mature and grow the amount of transactions increases, so does complexity, exponentially actually, due to their interdependence.

To this is constantly added complexity deriving from the environment it operate within, the influences of which can be severe. Businesses are powerless (most of times) to control environmental or market influences. Foreign policies, new laws, commodity prices, currency devaluations, your bigger customer going bust are only few events that can make things worse, that can undermine even the best of sale strategies, operational models or cash-flow projections.

Now you are going to argue that if these problems did not exist most of us would be out of business. This though is not the point I want to make. Where I want to direct your attention is to the way we tend to deal with these issues. What do we actually do to justify our daily rates compared to what we could possibly be doing?

Lets take it from the top.

There are several elements that affect the cost of these transactions. In relation to our customers' revenues the critical three (if we leave aside demand) are complexity, time deriving risk and currency exchange cost. These reduces their profitability between 8 and 83%. Happy to explain how I ended up with these figures even if I bet most of you have similar conclusions over the years.

Why? Because complexity needs management, processes and resources with the trio costing them enormous amounts of money. The mediators (the processors and the Banks) justify their charges with this exact argument.

Finally, currency exchange which similarly to time deriving uncertainty needs to be transformed into manageable risk elements and contingencies which in their turn need management, Insurance and Banks.

The three add up costing businesses $ 24 Trillion per year, with late and non-payments amounting to 4.8 T(European Payment Index) , the cost of Banking (without interest charges) to 18.5 T (Capgemini 2013) and the cost of insurance to anything between 1 and 3 T (ICISA) depending on the markets volatility .

And what we where doing about it when we are called, to try and save the day, by desperate businesses?

Lean Engineering to control complexity, mergers and acquisitions to achieve economies of scale, we design new processes based on our risk analysis were we often include the outsourcing organisations, we propose incentive schemes to reduce the probability of late or non payments capped with some “clever” Trade Credit Insurance and Currency hedging. To wrap it all up we propose often some form of an ERP coupled by supply chain controlling technologies and we tide the lot with some e-invoicing upwards and a bit of e-commerce downwards.

Right? Oversimplified but I believe accurate.

Do we believe that what we were doing will solve their problems long term? NO

We know that in any given transaction there are two parties. Our “influence” unfortunately is affecting only the one so, in the best of cases the end result is, mildly put, uncertain. Add to that the environmental influences I mentioned above and you have an improvement that can be shown only by the use of some well designed KPIs.

By giving expensive “medicines” to alleviate the symptoms do we actually believe we solved the problem? NO

But on the other hand that was not even a moral dilemma. Until yesterday that was all we could actually do or offer based on the theories and the models at our disposal.

Now, though, there are some alternative options. Now we can perform surgery instead of giving medicines to alleviate “pain”. We can tackle directly the root causes of the problems that businesses are facing.

Lets start from complexity.

Complexity derives from the actual amount of transactions and its cost grows exponentially. Over time the methods we used like Process Re-engineering, Lean Engineering, Business Process Management, CRM etc. failed to resolve the problem. They failed because they were not addressing the root cause, the fact that businesses despite their actual interdependence act as if they were alone. Even models followed by Dell or Apple or CISCO where transparency across the whole length of the supply chain is present the results are not the expected.

Take any supply chain you want in any field and start counting:

the impact that one may have on the rest when something out of the norm like a late payment or non payment happens. How many bottom lines upstream are going to be affected?

the amount of transactions happening between them upstream and downstream

the amount of resources needed to manage and support all these

the amount of processes we need to build, monitor and maintain in order to support them

the amount of IT systems we need, their supporting cost and the amount of software licenses we pay

….

There are Trillion of reasons to do something about it.

Let's take time.

Take again any supply chain in any field. From the moment you design your payment terms or you accept your suppliers' ones, risk arises. Risk, the management of which will inevitably lead the business to seek contingencies and reassurance. Do the insurers we use or the Banks, the Law firms, the Debt collectors, the currency hedging etc. were able to solve the problem? NO

Even business clusters that support JIT (just in time) production lines have the same issues.

Businesses keep eroding their profitability and keep adding cost because we are not addressing the root cause, the fact that businesses despite their actual interdependence act as if they were alone.

There are Trillion of reasons to do something about it.

So what can be done?

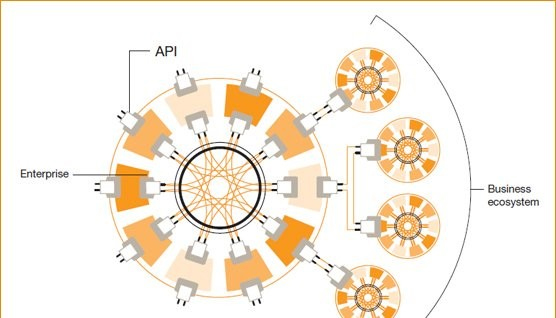

The answer is Two Dimensional Virtual Vertical Integration (2DVVI). The next generation model far beyond what Dell established some decades ago. In simple terms, follow a risk sharing strategy across the whole length of every supply chain a business is participate to. Where ever there are profound shared interests, common goals and inevitable interdependence perceive the chain as one organisation the functions of which are based on intelligent predefined and pre-agreed by the participants algorithms.

2DVVI can create business ecosystems that can act as one organisation WITHOUT affecting the independence of the businesses that constitute it.

Within such an environment where risk is shared none of the above described costs exist. A single transaction at the end of supply or value chain, based on these predefined and pre-agreed algorithms, can substitute all interim transactions, divide the payment to all participating businesses in the chain and update automatically accounting and ERP systems.

The three transactions (B2B plus Business to Bank plus Business to the Insurer) per node across a six levels supply chain, that until now were 15 are transformed into a single one.

As risk is shared time becomes irrelevant. Late and non-payments cease to exist as a notion. Human interaction with accounting systems becomes extinct. Liquidity increases exponentially over time and profitability can increase by up to 83%.

Is it applicable to all supply chains of any length you are going to ask? No, but it is in the majority. Even when applied to a single dimension supply chain with two nodes the economies of scale can improve liquidity by up to 100% and profitability by up to 33%. Yes, economies of scale are now possible to even the smallest of SMEs.

How all this “magical” stuff can happen?

My company is the first representative of a new generation of B2B-focused FINTECH enterprises that try to shake up with innovation-based technology the established ways in regards to the way business transact .

We built over the last two and a half years the infrastructure needed in order 2DVVI to become an easy to implement concept and the tools to complement the vast majority of cases even where cross border transaction occur and not only.

We built modular engines like Chain Payments, Parallel Payments or Enhanced Liquid Payments, Conditional Liquid Payments, Passive Risk Reduction or Private Virtual Banking…. or Bi-Directional Prepaid Cards our own mobile payment system and we keep building. We made last year's science fiction a reality.

However, there are two critical obstacles that we need to overcome:

while you may understand the above described concept we very much doubt that the average businessman does, and second that

we are addressing alone a 24 Trillion market and 100s of millions of businesses, which is mission impossible for any single company

So, we need your help.

We prepared the infrastructure and the tools to resolve once and for all the risk of late or non-payments and to reduce the need Factoring, Invoice Financing for Insurance, Currency Hedging and the rest. We can increase within weeks business cash-flow and increase their profitability. But we cannot do it alone.

We need you to tell the story and implement it.

We are seeking partners around the globe (our initial focus being Europe) to work with us. No consultancy is too small or too big to apply. If you like the idea or even if out of curiosity you want to know more give us a call.

You are not expected you to invest anything except customising your websites and marketing materials.

We will provide you with training and free access to our infrastructure. We will help you in building bespoke solutions if need be and support you technically all the way and at the post implementation stage where we will provide you with 2nd and 3rd line support.

We do not even expect to appear as a service provider if you do not want us to. White label propositions are welcomed.

Most importantly, we are prepared to share with you our profit and we do NOT expect you to do the same.

Interested?

Only a handful of applications will be accepted per country on a first come first served basis.

Multinational Consulting Firms will be considered on a regional level.

Our sites can be found at www.sonicesonice.com, and our platform that makes all possible at https://memeplex.es . You can contact us on info@sonicesonice.com.